This post is part of a series on College Savings Plans sponsored by CHET, the Connecticut Higher Education Trust’s 529 College Savings Plan. As always, opinions remain 100% my own.

Now that you have started a college fund and are saving money to it every month, what is the best way to invest for college? Read on to learn more about how to select the investment allocations for your child’s college fund, and the investment options offered by CHET that make meeting your investment objectives easy.

Over the last two months, I’ve outlined how you can set up your child’s college fund in as little as 15 minutes right online with CHET. Then, I showed you how easy it is to set up automatic contributions starting as low as $15 every pay period right from your paycheck. The next piece of the puzzle is determining the best way to invest the funds in your 529 plan in order to reach your long-term goal of paying for your child’s college education.

Every family’s investment objectives will vary. When setting the investment allocations for your child’s college fund, your objectives will be influenced by three primary factors: your investment horizon, your personal tolerance for risk, and your long-term savings goal.

Let’s examine what each of those factors means, how to determine what your specific preference is for each factor, and how you can use them to choose which investment allocations are right for your child’s college fund. And if all discussion of risk and returns makes your eyes glaze over, skip to the end to see how CHET Age-Based Investment Options make setting your investment allocations super easy for you.

The Best Way to Invest for College

By setting up a CHET 529 College Savings Plan, you have already chosen the right vehicle for investing for your child’s future college education. All the earnings on the funds in your plan can accrue, tax-free, until they are withdrawn. The earnings will remain tax-free forever, so long as the funds are used for qualified educational expenses.

But how do you decide which investment allocations are best for your child’s college fund? With tax considerations removed, you can focus your investment objectives on three primary factors:

- Your investment horizon

- Your risk tolerance

- Your long-term savings goal

These three factors work together to help you determine which investment allocations are right for you and your child’s college fund. Let’s examine each factor in more detail.

Defining Your Investment Horizon

With a college fund, determining your investment horizon is relatively straightforward. Most children go to school the year after they graduate from high school. That defines the investment horizon for your child’s college fund: you have from now until they go to college.

Those years define the investment horizon, or time period, you have to save and invest money to reach your college savings goal.

Your Risk Tolerance

Risk tolerance is a less black and white investment factor. Every family has a different appetite for risk. It can be personality driven, influenced by your overall household income and family wealth, but also may vary with your investment horizon.

Aggressive, Conservative or Moderate

Risk tolerance is typically described as aggressive, conservative or moderate. If you are an aggressive investor, you are willing to take on greater risk, for greater expected returns over the long run. This means your funds may go up and down more than the overall market.

The return is how much the value of your investment increases between your starting point and an end point. The movement up and down in between is known as volatility – aggressive investors are willing to stomach greater risk, measured as higher volatility, for greater expected returns. Note that I will always say “expected returns”. There are no guarantees when it comes to investing, so taking on higher volatility, also means exposing yourself to greater potential losses.

If you are a conservative investor, you prefer to have less variation and more certainty in your expected returns. You are more focused on preserving your funds, than generating outsized investment returns. This means your funds may go up less than the overall market (lower volatility), but your losses will also likely be less than the market. You accept lower expected returns, for less risk.

If you are a moderate investor, you lie somewhere in between.

A gambler likely has a higher risk tolerance than a penny pincher, who is likely more conservative. If you are trying to reach lofty savings goals relative to the money you can save every month, you may have to be more aggressive with your investment selections to make-up the difference.

Risk Tolerance vs. Investment Choices

So how do specific investment allocation choices align with risk tolerances? The answer is two-fold. There is a risk spectrum along which different asset classes fall, with equities (or stocks) being the riskiest, bonds being more moderate, and cash alternatives (more akin to a savings account paying interest) being most conservative.

However, within each asset class, there is also a range of risk. There are higher and lower risk equity investments: investing in the S&P 500 has lower volatility, than investing in a smaller cap index, like the Russell 2000. The same is true of bond investments. Investing in US Treasury Bonds is less risky than investing in higher yield, lower credit rating bonds.

By balancing your investment allocation choices across asset classes, no matter where you lie on the risk tolerance spectrum, you also add diversification to your fund portfolio, which reduces overall volatility as well.

Risk Tolerance vs. Investment Horizon

If you are starting a college fund for your baby, with years ahead of you to save, you can make more aggressive investment selections to help you build funds early, while you are also better able to recover from any losses. As they get closer to graduation, it is more important to have certainty in the funds available for college, so you will want to adopt a more conservative investment allocation to preserve your savings.

Long-Term Savings Goal

The final factor to consider when making your investment allocation choices is your long-term savings goal. College is expensive, and the cost of college is growing at a rate that outpaces income growth by multiples today. Establish a long-term savings goal for your child’s college fund that aligns with what you can afford and what you would like to contribute to their college education.

You will reach that goal through a combination of the contributions you make to the fund, as well as the investment returns generated by the money you save, and the years you have to save. You can use my Annuity Calculator to help you triangulate between how much you can contribute to your child’s college fund each year, the expected annual return, and your investment horizon.

CHET Investment Options

CHET offers four categories of investment options: single-fund, multi-funds, guaranteed and age-based. Single fund investment options are invested in a single fund, following a single specific market and/or strategy. Multi-fund investment options are invested across several different funds, achieving specific risk or asset allocation benchmarks (i.e. a balance between stocks and bonds). Guaranteed investment options are essentially providing only interest on your principal, much like a savings account.

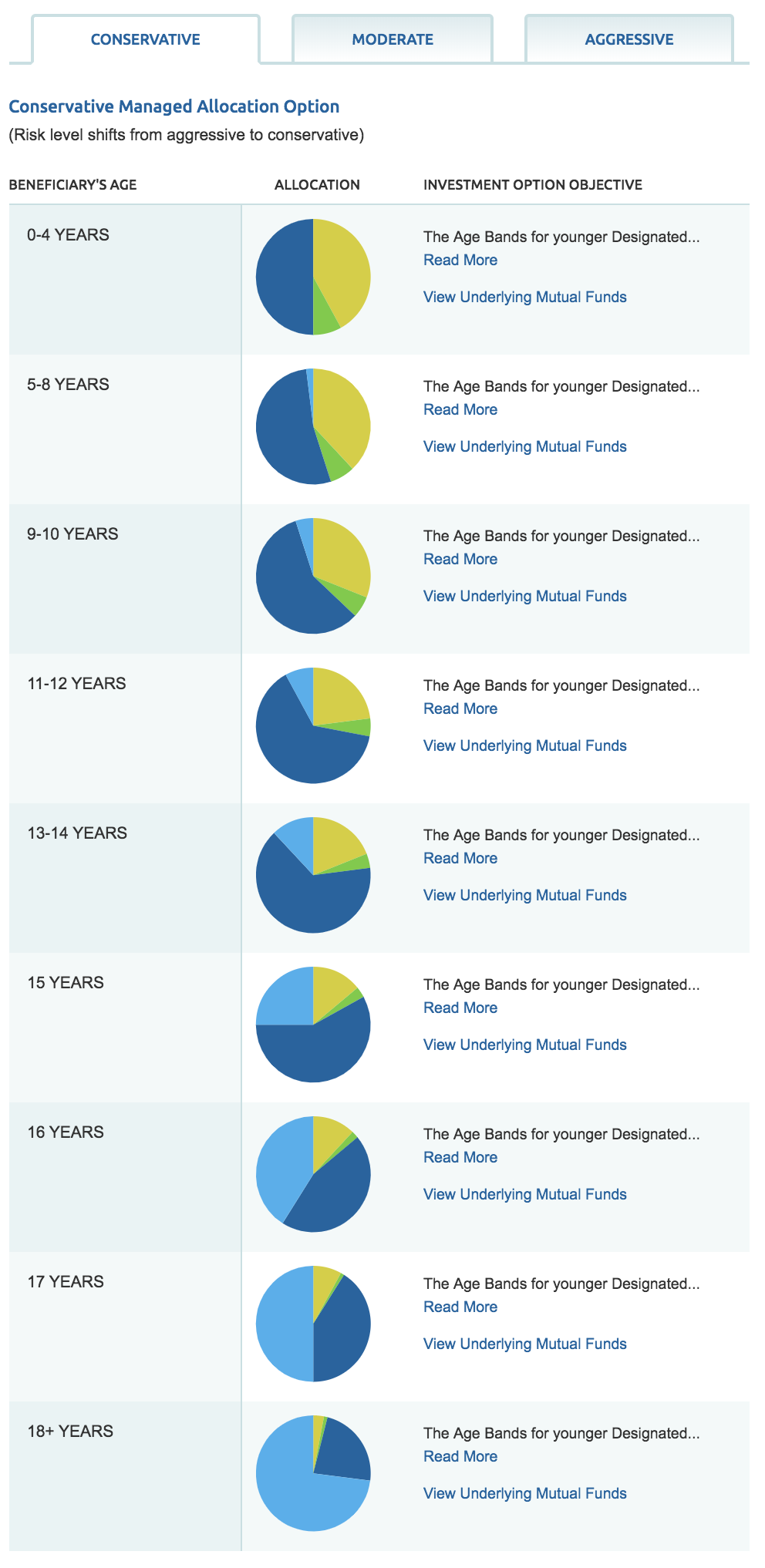

Age-Based Funds by CHET

Age-based funds are different from all of the other options. Age-based funds re-balance your asset allocations and investment choices for you based on your child’s age, with more equity exposure (higher risk, higher expected returns) the younger your child is and shifting to more bond and income based strategies (lower risk, lower expected returns and more preservation of capital) as your child near’s their high school graduation. If you choose an age-based investment option, you can choose an aggressive, moderate or conservative investment strategy that applies throughout.

This year, our middle child turned 5 in August. CHET automatically rolled her account from the 0-4 Years age band to the 5-8 Years age band. For families who want an investment solution that diversifies, re-balances and helps you reach your long-term investment objectives for your child’s college fund, given your risk preferences, Age-based funds are a great solution.

Understanding each of the different factors impacting your long-term investment objectives is complex – and the pressure is greater when you know the decisions you make can affect your child’s future. Hopefully, this helps you understand your risk factors and gives you greater confidence when making the investment allocations for your child’s college fund.

Be sure to catch the rest of my monthly CHET series! Start with how to set up a college fund, the best way to save money for kids college funds, and coming next month, just in time for the all those questions from the family about what to get your kids for Christmas – how you can allow others to contribute to your child’s college savings too! Follow me at Family Finance Mom on Facebook and Instagram to catch simple answers to your family’s money questions.

Love it? PIN THIS!

5 comments

[…] to a 529 account or an Educational IRA. It’s a simple and easy way to give a gift today that will help them in the […]

[…] […]

Oops meant ESA in my previous comment.

I had talked to a friend who is also in finance and she had suggested starting with an EPA instead of a 529 because you can use the money or more things. Just wondering your thoughts on the two types of college savings plans.

So I am less familiar with ESA’s, but ESA’s have more limitations than 529s, with two specific improved benefits. The benefits: 1) you can use the funds for K-12 education expenses, not just tuition. 529 withdrawals only permit K-12 tuition. 2) You can self-direct your investments with an ESA to a much broader range of funds, ETFs vs. just those offered by the manager of a 529. Those are the benefits.

The limitations are greater however – contributions are capped at $2,000 per year vs. up to and exceeding $300,000 maximum investment for 529s. Your ability to contribute to an ESA if you make over $190,000 a year jointly starts to phase out. There is no income restriction for 529 contributions. You also have to contribute to the ESA before the beneficiary is 18 and use it before they turn 30, while there are no age restrictions on a 529.

Initially, 529 plans only allowed for payment of higher education tuition and expenses – that left a hole for K-12 education tuition and related expenses that the ESA used to fill. Since then, 529 plans have expanded to allow for payment of K-12 tuition (though still not expenses).

The whole purpose of a college savings plan is to allow contributions to grow tax-free – if you are using it to pay for K-12 education, I’m not sure you get the same benefit of compounding, depending on the age of your child. Given that, I’d still opt in favor of a 529 plan. There are certainly individual circumstances (special needs, private education requirements, etc) that may make an ESA more valuable to specific families, but I would think that’s the exception, not the norm.

Hope that helps!