When I was 9 years old, the author/illustrator, Steven Kellogg visited my elementary school. My mom got me an autographed copy of a book he illustrated, If You Made a Million. I can’t tell you now if she bought it because I was already interested in math, or if the book is what peaked it, but I can tell you it cemented my fascination with numbers and finance, ultimately leading to my choice of college major and career. Having engrossed myself in the world of financial models, interest rates, returns, valuation, leveraged buy outs, and discounted cash flows for nearly a decade, and being married to someone in the same field, I often forget that basic financial concepts that are permanently burned into my brain are not so basic to the average person. Over the coming weeks, I will introduce various financial vehicles that every family should take advantage of – but before you can understand the benefits of those vehicles, you have to understand some basic finance, like Money and the Magic of Compounding.

Money and the Magic of Compounding

If You Made a Million is the perfect book to both introduce preschoolers and kindergarteners to the very basic concepts of money (you work to earn money, a nickel is five pennies, a dime is two nickels or 10 pennies, etc.), and as you read further, a great book to introduce more complex financial concepts, like interest, compounding, checks and mortgages, to older teens. It sill baffles me that basic financial concepts like, how to balance a checking account, and how credit cards and mortgages work are not part of most high school curriculum.

Interest Rates and Rates of Return

As the book describes, instead of saving your money in a piggy bank, where a year from now the dollar you put in will still only be $1, you can choose to put in a bank. Savings accounts provide the bank with assets, which the bank uses to make loans, like mortgages, to other bank customers. For use of your money, the bank pays you interest on your savings account. While the book talks about 5% annual interest rates, so your dollar today, would be worth $1.05 a year from now, interest rates today are at historic lows.

CDs, a type of savings vehicle where you agree to leave your money in place for a fixed period of time, did earn rates of 5% and even more up until the current century. Today, most savings accounts earn a fraction of a percent. The annual percentage yield (APY), a common way interest rates are quoted, on my current Money Market Savings account is 0.02%. Yikes – that’s barely better than leaving it in the piggy bank!

To earn better interest, you have to be willing to take more risk. Rates of return, be they interest rates on savings accounts or other fixed income instruments, like CDs or bonds, or investment returns on riskier assets like stocks, are supposed to be commensurate with the risk of loss associated with the investment. On a savings account, the chances of you losing all your money is essentially zero – even if the bank goes out of business, most bank deposits are now federally insured so your money is protected. Similarly, the interest you earn on a savings account is very low.

Magic of Compounding

Even at low rates of return, compounding still grows your savings over time. If there is a $1,000 in my Money Market Savings account today, a year from now, with an APY of 0.02%, I will have $1,002 in my account. After 10 years, at the same interest rate, $1,020. That doesn’t seem very magical…

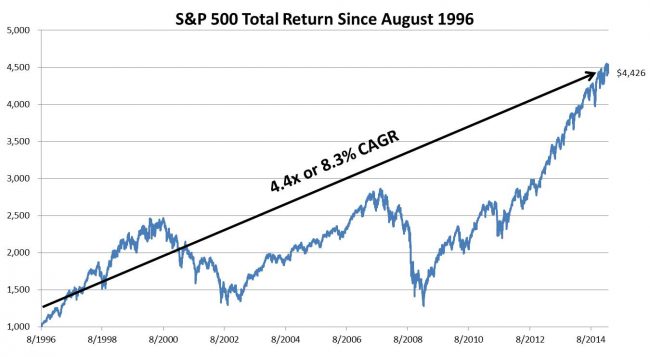

Let’s take a little more risk. Instead of sticking money in a savings account earning pennies a year, let’s invest in the stock market. As a proxy, we will use the total return for the S&P 500, a basket of the 500 largest stocks on the major US stock market exchanges, the NYSE and NASDAQ. Back in the summer of 1996, I had my first summer job – I nannied for two little girls to raise money to pay for cheerleading my freshman year of high school. I spent the hard-earned money on cheerleading camp, uniforms and monogrammed accessories. And my parents taught me a great life-lesson about the value of a dollar, making sacrifices, and working for what you want in life. But what if I had saved $1,000 that summer and invested it in the S&P 500 instead of spending it all on polyester uniforms, hair bows, monogrammed bloomers and duffle bags… what would it be worth today?

Over the last 18.5 years, the S&P 500 had a total compound annual return, often referred to as a compound annual growth rate (CAGR) of 8.3%. That means, if you look at the start and end points, ignoring all the ups and downs in between, my money compounded at 8.3% annually. The $1,000 I saved and invested at the end of the Summer of 1996, would be worth $4,426 or 4.4x my original investment. It was not without risk. There were periods of time over which I would have lost money when the stock market experienced steep declines (DotCom bubble burst in the early 2000s and the Housing Bubble Burst Great Recession of the last decade). However, ultimately, over time, I would have earned a substantial return. And it sure beats $20 every decade! Note: as any financial disclaimer will tell you, past returns are not a promise, nor indicative, of future returns.

Debt Compounds Too

It is important to note, that debt on which you pay interest has a similar compounding effect – only the benefit is to your creditor and the detriment is to you. The interest you pay on a credit card is far more expensive than most returns you will find in the stock market too. According to CreditCards.com, the national average annual interest rate (APR) on credit cards is nearly 15%, nearly 2x the annualized stock market return of the last two decades. That means, a $1,000 credit card balance, will cost you $150 in annual interest charges. And don’t miss a payment or violate any of the terms, or that rate can dramatically skyrocket to well over 20% or more.

The same is true of mortgages, although because they are supported by a valuable asset, your home, the interest rate is much lower, and currently, persist at historically low levels. As of yesterday, according to Bloomberg, the average 30-year mortgage rate was 3.69%. However, over 30 years – that adds up to a lot. In our town, the median home price is $260,000. If you buy a home at that price, with a 30-year mortgage at 3.69%, you will make 360 monthly payments of $1,195.27. After 30 years, you will have paid off your mortgage, with payments totaling over $430,000 for your $260,000 home purchase.

Monthly Payment Math

Don’t be fooled by this gimmick often used by car dealers… they will headline an advertisement or a commercial with a car sold for a “monthly payment of just $299.” What the fine print and speedy voice over doesn’t tell you is that requires a) a perfect credit score, b) a 6-10 year car loan, c) a HUGE down payment, d)a sizable interest rate, or e) all or some combination of the above.

I will never forget how many places my husband dragged me when he was shopping for his current car. The worst, by far, was to go to a dealership in the Bronx because they advertized a crazy deal on a Tahoe LTZ. If a deal seems to good to be true, it probably is… After we arrived, they took us in their car to a garage that seemed miles away, and showed us countless cars, none of which were the advertized, fully-loaded model or for the price indicated. When we didn’t seem fooled, they sat us down in the office with their “Finance Manager,” who hacked away at a black screen with green text, and repeatedly asked us “How much do you want to pay per month?” At one point, he offered us a $350 monthly payment, and when he showed us the screen it was for a 10 year car loan at over 9% interest. It was at that point that we finally got up and left.

Before you make any purchase with financing involved, you should understand 4 things: the purchase price, the financing cost, the term of the financing (how many months, years), and the required monthly payment. If you have any 3 of those items, you can determine the fourth. Without getting into complicated finance formulas, excel will calculate these for you using the PMT, NPER, RATE, and NPV formulas. Be sure to match the inputted interest rate with the period. For example, most interest rates are quoted on an annual basis (10% APR), but payments are made monthly, so your interest rate input would be 10%/12 and your periods would be the number of years x 12.

Other Factors

There are other factors at play here in the real world – namely taxes. The government collects taxes on all income, including income from investment returns and interest on savings accounts. The good news for investment returns: 1) taxes are only payable on realized returns, meaning as long as you don’t sell an investment, and your money remains invested, your taxes are deferred until you actually cash out, and 2) there are many college savings and retirement vehicles that provide tax advantages and deferrals as well. I will explain several of those in more detail over the coming Fridays. Conversely, interest payments on mortgages are also tax deductible (for now).

Are you amazed by the magic and magnitude of the impact of compounding? Do you have more questions about this basic financial building block? What other financial topics would you like to see me address? For more Financially Savvy posts, be sure to follow our Pinterest board!

Follow Meghan @ PlaygroundParkbench’s board Financially Savvy on Pinterest.

Disclaimer: This post is provided for education and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The information provided is general in nature and is not specific to you or anyone else. YOU SHOULD NOT MAKE ANY DECISION, FINANCIAL, INVESTMENTS, TRADING OR OTHERWISE, BASED ON ANY OF THE INFORMATION PRESENTED ON THIS SITE WITHOUT UNDERTAKING INDEPENDENT DUE DILIGENCE AND CONSULTATION WITH A PROFESSIONAL BROKER OR COMPETENT FINANCIAL ADVISOR. You understand that you are using any and all information available on or through this site AT YOUR OWN RISK.

5 comments

[…] Related Post: Money and the Magic of Compounding […]

[…] can set them up with a savings account with BusyKid. As they get older, you can even teach them the concept of compounding to motivate even more […]

[…] you start saving for college, the more money you will save and earn interest on (learn more about the magic of compounding). The last item on your baby financial checklist is to start a college savings plan, known under […]

Lots to take in there – thanks for sharing 😉

Thanks for linking up with #FabulouslyFrugal this week x x

[…] on Financially Savvy Friday, I am expanding on last week’s lesson on compounding. Now that you understand the magic of compounding, over the next few weeks I will outline […]